IDFC FIRST BANK FULL ANALYSIS 2025

HISTORY

IDFC FIRST Bank was established by the merger of erstwhile IDFC Bank and Capital First on December 18, 2018.

IDFC

IDFC Limited, a successful institution initially conceptualized for infrastructure financing in 1997, later diversified its operations. It ventured into investment banking and institutional securities in 2007, launched its mutual fund business in 2008, and introduced an Infrastructure Debt Fund in 2015.

CAPITAL FIRST

Capital First was established in 2012 through the leveraged buyout of an existing NBFC, with a singular focus on financing small entrepreneurs and consumers who were largely unbanked in India. Over 8.5 years, the company achieved remarkable growth, expanding its loan book from ₹94 crore to ₹29,625 crore. It recorded a 5-year CAGR loan growth of 29% and a profit CAGR of 56%, culminating in a net profit of ₹327 crore for the year ended March 31, 2018.

AFTER THE MERGER

Before the merger, IDFC Bank primarily focused on corporate banking. post-merger, IDFC FIRST Bank inherited exposure to distressed entities such as Dewan Housing Finance Corporation Limited (DHFL) and Reliance Capital. This exposure created challenges for the merged entity, with the total exposure amounting to approximately ₹1,784 crore. As a result of its exposure to distressed entities like DHFL and Reliance Capital, IDFC FIRST Bank reported a pre-tax loss of ₹417 crore in Q4 FY19. The bank increased its total provisions to ₹1,097 crore, covering 75% of the principal outstanding. This period was marked by consecutive quarterly losses. Simultaneously, the bank began transitioning from its legacy focus on corporate banking to becoming a retail-focused bank, laying the foundation for a more stable and diversified business model.

Liability Diversification During and After the Merger:

As of December 31, 2018, IDFC FIRST Bank had institutional borrowings and deposits totaling ₹1,08,020 crore, while retail deposits stood at ₹10,400 crore. Under the leadership of MD and CEO V. Vaidyanathan, the bank successfully diversified its liabilities. By March 31, 2020, retail CASA and term deposits had risen to ₹20,710 crore, a 157% increase from ₹13,214 crore. By 2020, retail deposits further grew to ₹33,924 crore. As of 2024, retail deposits have reached an impressive ₹1,75,300 crore, showcasing the bank’s strong focus on retail growth and stability.

NPA MANAGEMENT

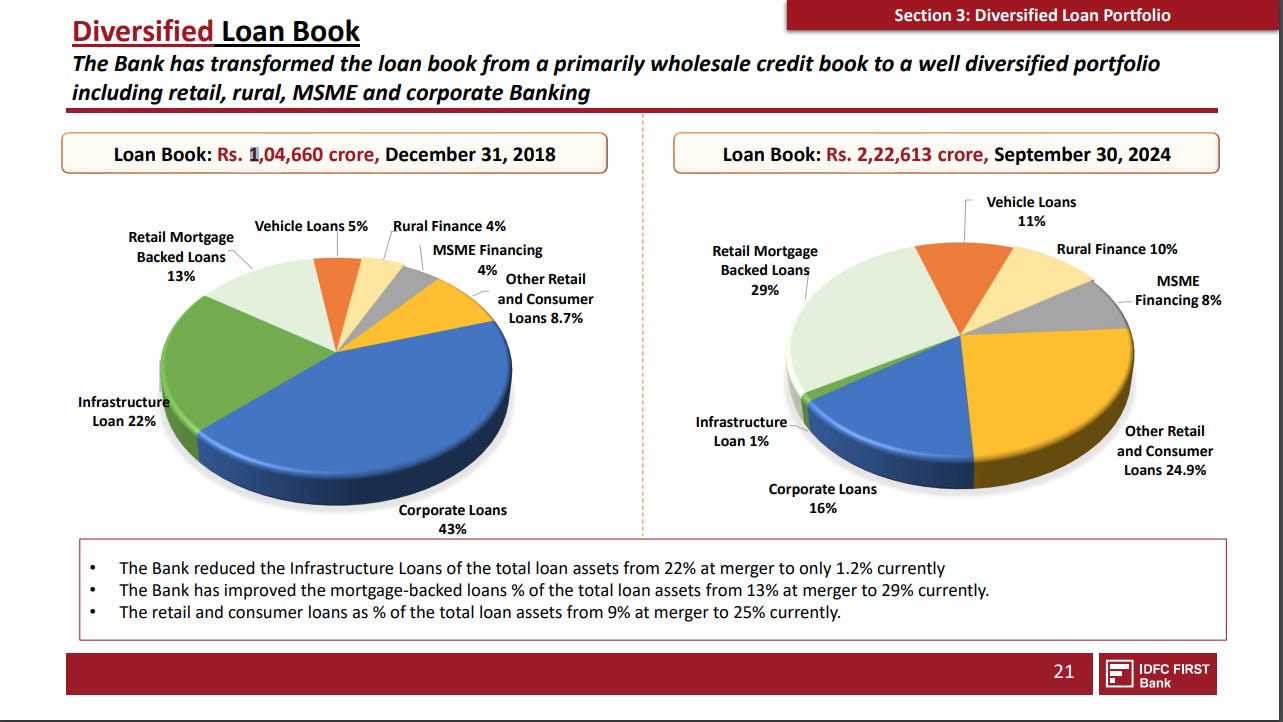

In 2020, IDFC FIRST Bank raised ₹2,000 crore in equity capital, strengthening its balance sheet. Leveraging its growing base of strong retail deposits, the bank strategically worked to reduce its infrastructure loan book. As of 2019, infrastructure loans constituted approximately 71.2% of the total loan book. By 2024, this figure was impressively reduced to just 1%, reflecting the bank’s successful transition toward a more retail-focused and diversified loan portfolio.

Q2 FY25 ANALYSIS

MICRO FINANCE AND TOLL ACCOUNT

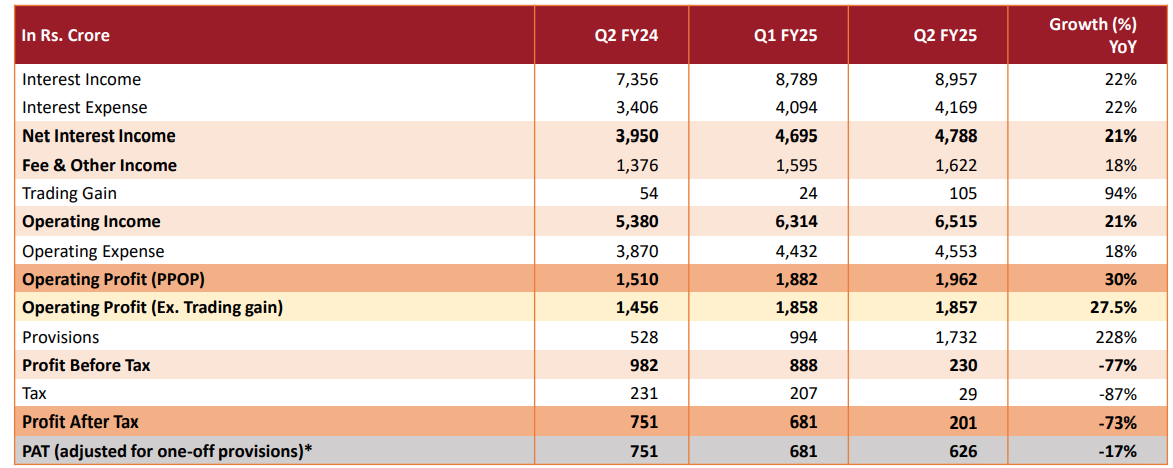

In Q2 FY25, IDFC FIRST Bank reported a profit of ₹212 crore, reflecting a year-on-year decline of 252%. The primary reason for this decrease was the stress in the microfinance segment and a legacy infrastructure toll road account. To address these challenges, the bank made provisions of ₹315 crore for the microfinance segment and ₹253 crore for the toll road account, significantly impacting profitability. If we exclude the provisions made for both the microfinance segment and the legacy infrastructure toll road account, the profit after tax (PAT) for the current quarter would have been ₹626 crore.

Q2 FY25 FINANCIALS

Interest income for IDFC FIRST Bank increased by 22% year-on-year, rising from ₹7,356 crore in Q2 FY24 to ₹8,957 crore in Q2 FY25. Operating income grew by 21% YoY, while operating profit impressively increased by 30% YoY. However, total provisions for the quarter stood at ₹1,732 crore, reflecting a 228% increase, primarily due to additional provisions made for the microfinance segment and the toll road account. As a result, the profit after tax (PAT) declined by 252% YoY, largely driven by these increased provisions. Despite the decline in PAT, the bank performed well overall in the quarter. The retail loan book grew by 25.1%, while the corporate loan book grew by 20%. Retail deposits saw strong growth, increasing by 37%, reflecting a healthy growth trajectory. The bank's Net Interest Margin (NIM) stood at 6.2%. However, the cost-to-income ratio remains relatively high at 70%, which is an area for improvement. The management has guided that they aim to lower this ratio in the upcoming years, and progress in this area will be closely monitored. Other key ratios include a Gross Non-Performing Asset (GNPA) ratio of 2.02%, a high CASA ratio of 48.9%, and a Return on Assets (ROA) of 1.2%.

MANAGEMENT

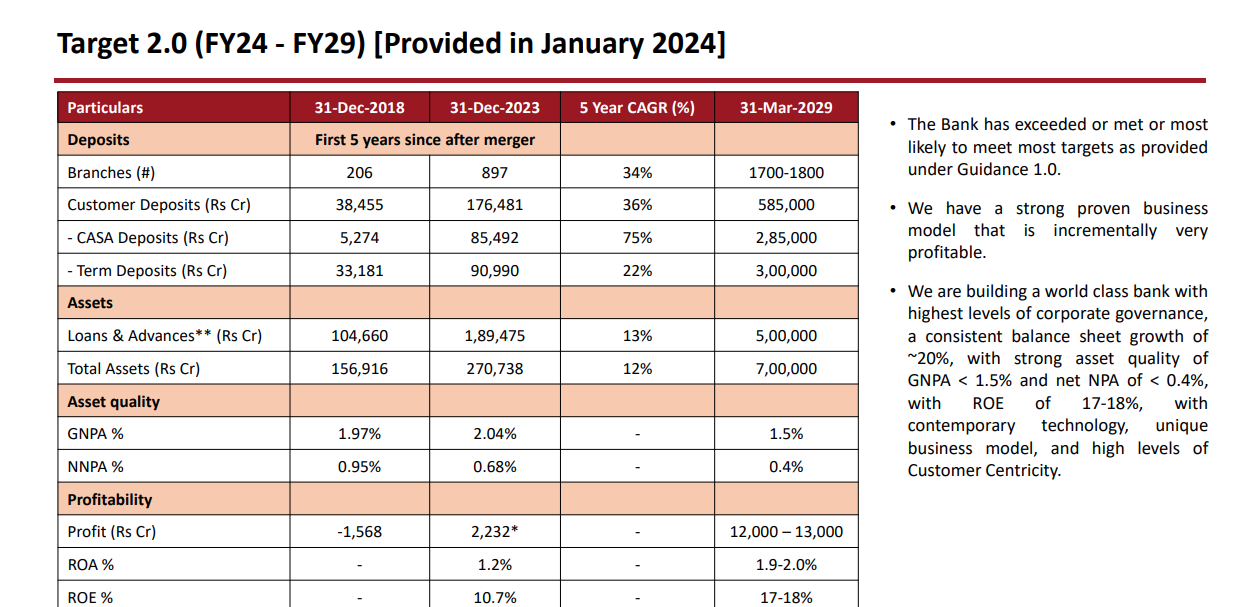

IDFC FIRST Bank's main asset is its strong management, primarily led by V. Vaidyanathan. If we look at their quarterly and annual reports, the bank provides a five-year guidance for investors, outlining their strategic goals and aspirations for the coming years. This offers investors a clear view of where the bank is aiming to go in the next five years. Below is the guidance picture of IDFC FIRST Bank.

VALUATION

The current price-to-book (P/B) ratio of IDFC FIRST Bank is 1.42, while the median P/B ratio of the bank is 1.6. At this range, the bank is not considered undervalued, but rather fairly valued.

Key things to note in history of IDFC first

1) it's been over 6 years, while bank hasn't been able to normalize cost to income ratio - please look at other expense breakup in ipex to have more insights

2) VV has been changing C2I goal posts since 2 years( refer to concalls starting q2FY23 till date)

3) since roe is less(primarily because of high c2i) while growth of loan book is higher than roe, it's CAR continue to deplete every 3-4 qtrs and hence frequent fund raise has led to very high equity, and this will continue till roe doesn't increases above growth or growth doesn't slows down below roe

4) past 16 qtrs, whenever a provisioning is taken as contingency, it's has silently been pushed into retail book in following quarters by writing it back in the segment while creating a new one against retail assets, while showing no net impact in quarterly results while the blame being continuosly given to legacy book.

5) thesrecent provision of toll account - has been there since 5-6 years on the book and didn't needed any provisioning, you will see it being written back and adjusted into other business vertical

6) VV never answers retail investors questions properly and tell them to shift to other shares if u r unhappy - no minority protection here

7) whenever bank prices fall, he gets issues lot of esops, which he sells off for some or the other reason when the prices are doing well.

8) their actual NIM is not that high which is being quoted because their DSA agent fee is below the NIM calculation

Happy to have a longer discussion.

Thanks sir for detailed information very helpful please keep doing sir 👍❤️